According to Business Wire, OpenFX uses stablecoins as an intermediary settlement layer for near-instant FX conversion and cross-border payments, with more than 98% of transactions on the platform settled in under 60 minutes (Source: Business Wire, March 31, 2026). This model differs from the approach based on central bank digital currencies (CBDCs). CBDCs involve the issuance of a settlement asset by a government regulator; therefore, their cross-border application depends on intergovernmental agreements, legal recognition, and the willingness of foreign participants to connect to another central bank’s infrastructure.

Private FX platforms rely on a different logic. The client can remain within the familiar fiat framework, while the stablecoin is used within the payment chain for currency conversion, routing, and settlements between local payment channels. OpenFX reports support for more than 40 currency pairs, over 25 local payment channels, and 24/7/365 operations (Source: OpenFX, 2026).

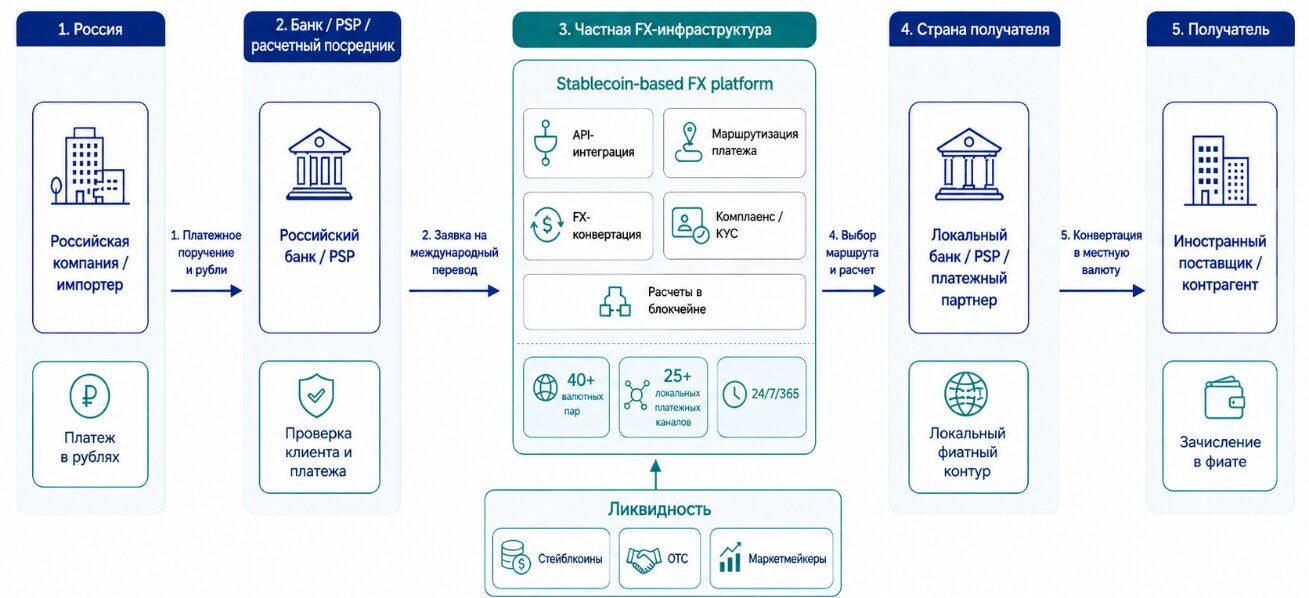

The significance of this model lies in the fact that the platform combines several functions that, in the traditional scheme, are distributed among correspondent banks, FX intermediaries, local payment systems, and other participants in payment relationships. It selects the settlement route, provides access to liquidity in the required currency pair, performs conversion via a stablecoin, and transfers funds into the recipient’s local fiat environment.

For the paying company and the foreign supplier, this reduces the need to independently work with crypto wallets or blockchain infrastructure. The digital asset is used within the payment route as a value transfer instrument between different currency zones, while the final recipient may receive funds in a familiar fiat form.

A similar mechanism is used by Circle in CPN Managed Payments, where a stablecoin is embedded into the payment infrastructure, allowing a bank or fintech company to handle settlements without independently holding digital assets or building its own blockchain infrastructure. However, the emphasis of these models differs. Circle builds infrastructure around USDC and assumes responsibility for issuance, redemption, routing, compliance, and technical support of settlements. This scheme is convenient for participants who need access to stablecoin settlement through a single issuer and a single settlement asset.

OpenFX focuses on FX infrastructure, liquidity, and the connection of different currency environments via API. For foreign trade settlements, this may represent a more flexible model.

A simplified scheme of a cross-border payment using private FX infrastructure based on stablecoins is shown in Figure 1.

Figure 1. Cross-border payment scheme via private FX infrastructure

In this model, the digital asset is used within the payment route as an intermediary settlement layer, while the sender and the final recipient may remain within their familiar fiat environment.

For Russia, such solutions are of interest as a technological alternative to dollar-centric infrastructure, especially amid increasing complications in cross-border payments. However, the direct use of Western stablecoin and FX platforms is limited by sanctions, compliance, and jurisdictional risks. Therefore, it is the architecture of such a model that is of particular interest; the market requires private settlement platforms capable of integrating national currencies, liquidity in digital assets, local payment channels, and participant verification procedures.

Author: Assistant Lecturer, Department of World Economy and International Finance, Financial University under the Government of the Russian Federation, Nikita Dmitrievich Klevanets.